REACH was a stress test. Here is what broke.

A health system operator’s read on the PY2023 evaluation.

The ACO Realizing Equity, Access, and Community Health model was never supposed to be a permanent program. It was a four-year test, running from PY2023 through PY2026, redesigned out of the Global and Professional Direct Contracting model that ran under the previous administration. The stated purpose was to pull more Medicare fee for service beneficiaries into accountable care relationships, test whether aggressive capitation and risk sharing could bend the cost curve, and prove that providers, not investors, should govern the entities taking that risk.

Three and a half years in, with the Center for Medicare and Medicaid Innovation’s PY2023 Preview of Findings now public, we finally have enough data to say something honest about what REACH did and did not prove. The answer is not tidy.

REACH is neither the breakthrough its advocates want nor the failure its critics assume. It is a stress test that exposed exactly which parts of the value-based care thesis hold up under real world conditions and which parts bend.

What CMS asked REACH to do

Underneath the equity framing, REACH was built to answer three operational questions MSSP and Next Generation ACO had not fully resolved.

1. Could full risk capitation, delivered through either Primary Care Capitation or Total Care Capitation, fund enough upstream care redesign to produce durable savings?

2. Could the model attract and retain organizations that serve genuinely complex populations, the kind of patients MSSP participants have historically been accused of avoiding?

3. Could CMMI impose provider governance and beneficiary vetting rules strict enough to prevent the investor driven gaming that surfaced in GPDC without driving participation to zero?

The design reflected all three bets. Participants chose between the Professional Option, sharing 50% of savings and losses with Primary Care Capitation, and the Global Option, taking 100% of risk with a discount applied to benchmarks. That discount was 3% in PY2023 and PY2024, rising to 3.5% in PY2025 and 4% in PY2026. The tiered ACO types, Standard, New Entrant, and High Needs, were meant to make room for different sizes and missions. High Needs ACOs only needed 1,000 aligned beneficiaries to participate, compared to MSSP’s 5,000 minimum, which was a deliberate accommodation for frail, dual eligible, and chronically ill populations.

What happened

In PY2025, 103 ACOs were participating, serving roughly 2.5 million traditional Medicare beneficiaries through 161,765 providers. Ninety chose the Global Option. Thirteen chose Professional. The composition matters more than the totals. REACH attracted a self-selected pool of operators willing to take full downside risk on a new federal model, and almost all of them came from three clusters.

Physician enablement companies with Medicare Advantage muscle like agilon health, Aledade, and Privia.

Dedicated high needs operators in the ChenMed, Oak Street, and Iora lineage.

And a smaller set of integrated health systems running REACH as a strategic experiment adjacent to their MSSP operations.

Whatever REACH proved, it proved it specifically about these three clusters, not about the median American health system.

The PY2023 evaluation surfaced three findings a health system leader should not gloss over.

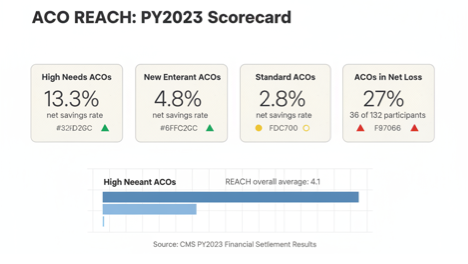

The first is the headline: High Needs ACOs averaged a 13.3% net savings rate. Standard ACOs averaged 2.8%. New Entrant ACOs landed at 4.8%. REACH ACOs overall averaged 4.1% across all tracks, with individual ACOs ranging from negative 15% to positive 25%. A five times gap between tracks inside the same model is the kind of differential that would normally force a conversation about whether the result reflects model design or operator selection. CMMI’s preview report largely attributes it to model design. A skeptical policy reader would note that the fourteen High Needs ACOs in the sample were heavily weighted toward operators with existing Medicare Advantage experience, prior Programs of All Inclusive Care for the Elderly (PACE) exposure, or both. The honest interpretation is that REACH validated the high needs thesis and the experienced high needs operator thesis simultaneously, and the evaluation design cannot fully separate the two. New Entrant ACOs averaged 4.8% net savings, sitting between the two, which suggests the performance gap is a gradient tied to population complexity and operator experience rather than a clean binary between tracks.

The second finding is that Standard and New Entrant ACOs showed improving gross spending reductions in PY2023 relative to prior years, with statistically significant reductions for New Entrants, but cumulative estimates across all ACO types still show Medicare fee for service net spending increasing under the model once shared savings payouts are netted out. The polite reading is that the model is trending in the right direction and needs more time. The less polite reading is that three years in, CMMI is still paying out more in shared savings than the model is reducing in spending, and the burden of proof for continuation sits squarely with the advocates of the thesis.

The third finding is the one that gets underreported. Thirty six of the 132 ACOs participating in 2023 took net losses. That is 27%, more than a quarter of participants. The question worth asking is not whether losses are acceptable in a full risk model, because they obviously are, but whether the benchmark discount methodology produced losses that were structural rather than performance based. CMMI’s decision to adjust the PY2026 financial methodology suggests they believe at least some of the losses were structural. If that is right, the model was testing two things simultaneously, care redesign capability and benchmark tolerance, and some participants failed the second test while passing the first.

One methodological note worth holding. The financial settlement numbers cited above come from CMS’s PY2023 financial settlement results. The CMMI evaluation produces separate estimates using a different methodology, and the two sets of numbers do not always match. PY2022 showed $632.2 million in evaluation losses compared to $855.6 million in savings relative to benchmark, which is the kind of gap that forces honest analysts to cite both and let readers judge. I am using the financial settlement numbers here because they are the ones health system leaders are most likely to encounter in trade press coverage, but the full evaluation report expected later in 2026 will give us a second lens.

The question the evaluation does not answer

The PY2023 preview is careful, but it leaves one question hanging any serious policy reader will immediately notice: How much of REACH’s High Needs performance is attributable to the model versus to the operators who chose to participate in it? Sensitivity analyses in the evaluation removed beneficiaries served by other accountable care programs from the comparison group and produced more favorable total gross spending reduction estimates, which is suggestive but not conclusive. Until the full evaluation report resolves this selection question, anyone citing the 13.3% number as proof that LEAD should replicate REACH’s high needs design is running ahead of the data. I think the design bet is still the right one. I also think we should be honest that the evaluation has not closed the case.

What this actually tells us

Three conclusions seem defensible.

REACH proved provider governance and beneficiary protection rules can coexist with full risk participation. Despite the stricter oversight regime imposed after GPDC, 103 ACOs stayed in the model and most chose the hardest risk track. That is not nothing. It is a counterexample to the view that CMMI cannot run a model without either letting investors run wild or driving participation away.

REACH proved the high needs thesis is the strongest thesis in value-based care, pending resolution of the selection question. The five times performance gap between High Needs and Standard ACOs is the single most important finding in the evaluation, and if the full report confirms the design attribution, it will shape the next decade of CMMI model architecture

REACH did not prove aggressive capitation produces net savings for Medicare at the program level. It is possible future performance years will change this. It is also possible they will not. An honest operator must hold both possibilities at once.

The REACH evaluation is the reason LEAD exists in the shape it does. CMMI did not wake up one morning and decide accountable care needed rebranding. The financial methodology adjustments coming in PY2026, the continued investment in the High Needs track concept, the carryover of benefit enhancement incentives like the Substance Access BEI into LEAD, all of these are CMMI responding to specific findings from the evaluation we just walked through.